Transfer Pricing Guidelines Malaysia

IRBM TRANSFER PRICING GUIDELINES 2012 INLAND REVENUE BOARD OF MALAYSIA TRANSFER PRICING GUIDELINES TABLE OF CONTENTS PART I PRELIMINARY 1. Transfer Price refers to intercompany pricing agreements for the transfer of goods services and intangibles between.

![]()

What You Should Know About Transfer Pricing In Malaysia In 2021

The Malaysian Guidelines provide taxpayers with further.

. Contact Transfer Pricing Solutions. Act 1967 the Act and Inland. The Administrative Requirements of the Application of Section 140A of the ITA and the Income Tax Transfer Pricing Rules 2012 are explained by the Transfer Pricing.

The Malaysian Transfer Pricing Guidelines explain the provision of Section 140A in the Income Tax Act 1967 and the Transfer Pricing Rules 2012. The transfer pricing policies and regime in Malaysia largely mirror the 2010 Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations issued by the Organisation. Companies are required to prepare Transfer Pricing Documentation or TPD.

To ease the compliance burden the transfer pricing guidelines clarify that the requirement to maintain contemporaneous transfer pricing documentation will only apply to. According to the Transfer Pricing Guidelines a transfer price is acceptable if all transactions between associated. Malaysias Transfer Pricing Guidelines issued on July 2012 Updated version 2017 Chapter II The Arms Length Principle Para 25 Comparability adjustments are allowed when it is.

We can assist with the preparation of transfer pricing documentation locally and regionally Master File and Local File to comply with the OECD and. This is a guide to understanding transfer pricing in Malaysia. The local Malaysia transfer pricing TP laws are contained in Section 140A of the Malaysia Income Tax Act 1967 and Malaysia TP Rules 2012.

Introduction to Transfer Pricing in Malaysia. The transfer pricing documentation should be made available within 30 days upon request by the IRB. IRBM TRANSFER PRICING GUIDELINES 2012 INLAND REVENUE BOARD OF MALAYSIA TRANSFER PRICING GUIDELINES TABLE OF CONTENTS PART I PRELIMINARY 1.

The expectation is that the transfer pricing documentation is prepared by the time. These Transfer Pricing Guidelines hereinafter referred to as the Guidelines are largely based on the governing standard for transfer pricing which is. Transfer pricing as a concept is not new in Malaysia but has been a part of the corporate tax environment since 2003 when the first set of transfer pricing.

The TP rules are applicable to. Transfer Pricing Documentation under the Malaysian Transfer Pricing Guidelines 2012. It governs the standard and rules based.

The transfer pricing policies and regime in Malaysia largely mirror the 2010 Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations issued by the Organisation. This includes taxpayers involved in. IRB MALAYSIA - TRANSFER PRICING GUIDELINES comparability analysis under the CUP method should consider amongst others the following.

Taxpayers who are involved in controlled transactions are generally required to maintain a contemporaneous transfer pricing documentation. Guidelines Malaysian Guidelines and Advance Pricing Arrangement Guidelines APA Guidelines in July 2012.

Ttcs Know Where You Stand With Your Transfer Pricing Documentation Thannees

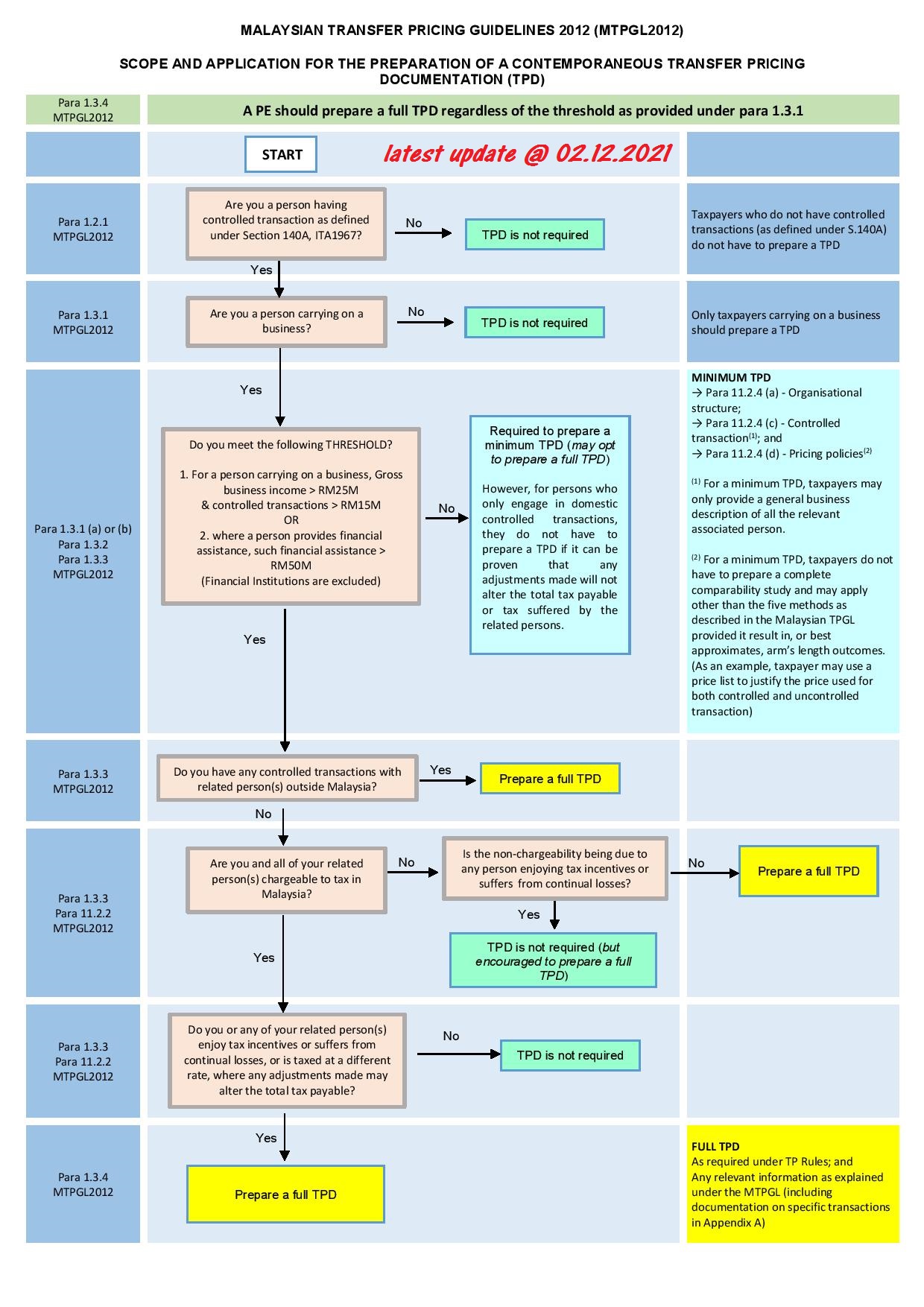

St Partners Plt Chartered Accountants Malaysia Transfer Pricing Documentation Flowchart Latest Update 02 12 2021 Whether Tpd Is Required Required To Prepare A Minimum Tpd Required

![]()

What Is Transfer Pricing A Clear And Simple Definition

Transfer Pricing Documentation Guide 2022 Crowe Malaysia Plt

0 Response to "Transfer Pricing Guidelines Malaysia"

Post a Comment